Once confined to science fiction, artificial intelligence (AI) has quickly developed into a potent force influencing our daily lives. AI is permeating every industry, revolutionising how we live, work, and interact in fields as diverse as healthcare, transportation, education, and entertainment. It is critical to carefully analyse this technology’s societal impact because it offers enormous potential and serious concerns at the same time.

Restructuring Industries:

The influence of AI in sectors like healthcare is one of its most significant. AI’s diagnostic systems may analyse large volumes of medical data, helping physicians develop more precise diagnoses and treatment regimens. It has the potential to lower healthcare expenses while greatly improving patient outcomes. AI-driven personalised learning platforms in education cater to each student’s demands, increasing engagement and memory retention. Additionally, AI algorithms optimise processes, offer tailored recommendations, and reduce fraud in finance and e-commerce industries.

Improved Accessibility:

For people with disabilities, AI is removing hurdles. Artificial intelligence (AI) allows voice-controlled interfaces and improves accessibility for those with visual impairments through speech recognition and natural language processing. Additionally, information is more widely accessible across languages and cultures thanks to AI-powered captioning and translation services.

Sustainability and Climate Change:

One of our time’s most pressing global concerns is the fight against climate change. AI is crucial in this conflict by maximising resource allocation, enhancing energy efficiency, and enabling disaster prediction modelling. Machine learning algorithms analyse environmental data to produce exact forecasts and create sustainable development plans.

Fairness, bias, and morality:

Bias and fairness become more of a concern as AI systems make more decisions in delicate fields like lending, hiring, and criminal justice. AI systems may unintentionally reinforce or exacerbate pre-existing societal biases if they are not carefully developed. Strong ethical frameworks must be implemented, and AI system prejudice must be regularly monitored and addressed.

Data Security and Privacy:

AI’s widespread use also prompts worries about data security and privacy. Because AI systems rely so heavily on data, securing it and using it ethically is crucial. A constant problem is finding the correct balance between using data for public benefit and preserving individual privacy.

Replacement of Jobs and Retraining:

The increasing deployment of AI and automation has raised concerns regarding potential job displacement. While some professions may be automated, new ones will certainly emerge that frequently require various skill sets. Participating in reskilling and upskilling initiatives is essential to ensure the staff can adjust to the crew’s changing needs.

Global Collaboration and Regulation:

International cooperation and regulation are essential as the impact of AI is worldwide. Establishing moral standards, frameworks for data sharing, and standards for the ethical creation and use of AI systems are all part of this.

Conclusion:

AI’s social impact is significant and diverse, and it can help with some of the world’s most urgent problems. We must, however, approach this technology with a mix of excitement and caution. We can fully utilise AI for the benefit of society by actively addressing ethical, privacy, and justice problems, as well as through international cooperation and prudent regulation. By doing this, we open the door to a time when artificial intelligence (AI) will be a force for good, fostering a more diverse, sustainable, and successful society.

Artificial intelligence (AI) in education in the digital era has resulted in a paradigm shift in how students learn and teachers impart knowledge. AI technologies can improve engagement, personalize learning, and close accessibility barriers. This article examines the different ways that AI is transforming education and influencing the way people learn.

Personalized Learning:

The idea of personalized learning is one of AI’s most significant contributions to education. Individual pupils’ various learning styles and paces are frequently difficult to accommodate in traditional classroom settings. AI-driven adaptive learning systems may examine students’ learning styles, strengths, and weaknesses to customize the curriculum to meet their needs. It guarantees that each learner has a unique learning experience, which improves understanding and retention.

Language Learning and Translation:

AI-powered language learning platforms can provide real-time translation, pronunciation assistance, and personalized language lessons.

Enhanced Engagement:

Chatbots and virtual tutors are two AI-powered systems that have improved learning through interaction and engagement. Instant responses from chatbots to questions produce a dynamic learning environment that mimics the speed of online discussion. Students can understand difficult ideas independently with one-on-one assistance from virtual tutors. These tools help learners develop a sense of independence, self-efficacy, and deeper understanding.

Smart Content Creation:

The creation of instructional content is also altering as a result of AI. Based on unique learning profiles, it creates tailored learning resources, such as quizzes, assignments, and study guides. It not only reduces the effort for teachers but also ensures that the information is tailored to meet the individual needs of every student. Additionally, AI-driven content production systems adjust to curricular changes to keep materials current.

Virtual Tutors and Assistants:

AI-enhanced chatbots and online instructors can help students by responding to their inquiries, explaining concepts, and offering study advice.

Data-Driven Insights:

With the help of AI, educators may now receive insightful knowledge on how well their students are performing. AI algorithms can pinpoint areas where certain students may be struggling or succeeding by analyzing data on student progress. Early intervention is possible because of this data-driven methodology, which enables teachers to support students and modify the curriculum promptly. Additionally, it aids in monitoring long-term development and adjusting teaching methods to enhance student learning.

Inclusivity and Accessibility:

AI-driven solutions can address accessibility gaps and increase diversity in education. For instance, students with hearing impairments or non-native English speakers can benefit from AI-driven transcription and translation services. To ensure that all students have equal access to educational materials, AI-driven content can also be modified to fit various learning difficulties.

Ethical Considerations and Challenges:

While incorporating AI into education has many advantages, it’s important to recognize the difficulties and ethical issues involved. These include worries about algorithmic bias, data privacy, and the necessity for continual professional development for educators to use AI technologies effectively.

Conclusion:

AI integration in education is a revolutionary improvement in how we approach learning. AI is revolutionizing education in several ways, including personalized learning, increased engagement, clever content production, data-driven insights, and greater accessibility. It’s critical to strike a balance as we advance between utilizing AI’s potential and resolving the ethical and practical issues that arise. By doing this, we can fully realize AI’s educational potential and improve the learning environment for all students.

The interpretability of models has become a crucial issue in the era of ever-improving artificial intelligence and machine learning. It is essential to comprehend how these models make decisions as algorithms get more complex and are used in high-stakes fields such as autonomous vehicles, banking, and healthcare. This knowledge promotes user confidence in AI systems and makes it possible to implement them successfully. We will examine this post’s fundamental components of interpretability, illuminating the approaches and strategies that connect machine learning to human comprehension.

1. Feature Importance:

Knowing which characteristics are important in making decisions is essential for a model to be interpretable. Assigning significance ratings to features using permutation importance, Shapley Additive explanation (SHAP), and LIME (Local Interpretable Model-agnostic Explanations) is standard practice. These techniques reveal which variables and how much they affect the model’s output.

2. PDPs (Partial Dependence Plots):

Partial dependence graphs display the connection between a component and the anticipated outcome when all other properties are constant. This visualisation technique aids in understanding the marginal impact of a single element on the model’s predictions and offers insightful information about how the model responds to particular variables.

3. Local Interpretable Model-agnostic Explanations (LIME):

LIME (Local Interpretable Model-agnostic Explations) is an effective technique for deciphering specific predictions from complicated models. It applies a local neighbourhood of the data point of interest to train a more basic, understandable model. This substitute model makes it simpler to comprehend why a specific prediction was made by roughly simulating the behaviour of the sophisticated model.

4. Shapley Principles:

Shapley values, rooted in cooperative game theory, assign weights to each feature’s contributions to the prediction. SHAP values provide a consistent framework for feature importance and interaction analysis in machine learning. They offer a more subtle knowledge of the complex interactions between various variables that affect predictions.

5. Decision Trees and Rule-based Models:

Decision trees and rule-based models are understandable. There is a direct connection between the input features, the predictions they provide, and the principles they use for doing to examine readily. Furthermore, techniques like rule extraction can convert complex models into comprehensible rules.

6. Model-Agnostic vs. Model-Specific Techniques:

Any machine learning model uses model-agnostic approaches like LIME and SHAP, regardless of the underlying architecture. On the other hand, some models better suit model-specific techniques (such as decision trees and linear regression). Slate complex models into easily understandable rules. The decision between these methods depends on the particular specifications of the current challenge.

7.Local Explanations vs. Global Explanations:

Both the local and the global contexts are used for contextualise interpretability. While international explanations offer insights into the model’s overall behaviour, local causes concentrate on understanding the model’s conduct concerning a single data point. It’s essential to strike a balance between the two to comprehend model behaviour fully.

Conclusion:

The concept of interpretability is not universal. It necessitates a nuanced approach that combines several techniques and procedures to meet the unique requirements of the problem and the model at hand. The foundations of interpretability will become increasingly important as machine learning permeates important domains to guarantee openness, responsibility, and trust in AI systems. By incorporating these methods into the machine learning process, we open the door to a time when AI judgements are correct and understandable to people.

Healthcare, economics, entertainment, and transportation are just a few areas of life that artificial intelligence (AI) has revolutionized. However, AI has a darker side that involves its nefarious application and enormous potential for good. This article examines the potential military applications of AI, its fresh dangers, and the urgent need for moral principles and regulatory frameworks.

1. Deepfakes and Synthetic Media:

Deepfakes are AI-generated pictures, sounds, or videos that mimic real-world human behaviour. They help to imitate persons realistically, frequently leading to incorrect information, damage to one’s reputation, and even financial fraud. For instance, deepfake films that use prominent individuals’ words and actions to spread lies or cause unrest have deceived celebrities, public figures, and average people.

2. Surveillance and Privacy Invasion:

AI-driven surveillance systems have allowed for unprecedented degrees of privacy invasion. State and non-state actors can track a person’s behaviour, analyze their voice, and recognize them using facial recognition software without the subject’s knowledge or permission. There are serious repercussions for civil liberties and worries about potential exploitation.

3. Cyberattacks and Advanced Persistent Threats:

Cybercriminals now have the means to carry out elusive and complex attacks thanks to AI-powered tools. Users may execute targeted phishing attacks, find system security holes, and even automate acquiring sensitive data using AI algorithms. Additionally, using AI in Advanced Persistent Threats (APTs) makes it possible for attackers to cause serious damage and remain undetected for a long time before discovery.

4. Social Engineering and Manipulation:

AI-powered algorithms can analyze massive volumes of data to produce highly targeted social engineering efforts. Malicious actors can adapt communications and content to target people’s weaknesses by understanding human behaviour and preferences. It becomes clearer during political elections, as artificial intelligence helps us spread misinformation and sow strife.

5. Systems for Autonomous Weapons:

Using AI in autonomous weapon systems raises significant ethical and security considerations. These computers might make split-second choices thanks to their sophisticated algorithms and machine-learning capabilities. This change, like combat, prompts concerns about responsibility, appropriateness, and the possibility of unforeseen effects.

6. Bias and Discrimination:

If not properly developed and educated, AI systems have the potential to reinforce and even amplify preexisting biases. It is clear in methods for loan approval, predictive policing, and recruiting algorithms. Biassed AI causes systemic prejudice, which reinforces societal inequity.

Conclusion:

Malicious use of AI puts people, organizations, and society in obvious and present danger. As AI technology develops, ethical issues, legal frameworks, and strong security measures must be implemented to decrease these risks. Cooperation between governments, industry leaders, and researchers is crucial to guarantee that AI is used for the good of humanity rather than its detriment. By working together, we can only expect to manage the complex environment of AI’s potential for both good and damage.

The combination of artificial intelligence (AI) and machine learning (ML) has shown to be a powerful force for change in the face of growing environmental issues. These technologies are bringing about a paradigm change in the way we think about sustainability and providing fresh answers to challenging ecological matters. AI is transforming several industries by leveraging data and sophisticated algorithms to promote more effective, efficient, and sustainable practices.

The Influence of Data:

The capacity to process and analyze enormous amounts of data is at the core of AI’s impact on sustainability. Complex, interrelated variables, from climate change to biodiversity loss, characterize environmental problems. The complexity and sheer volume of data needed to comprehend and effectively address these difficulties are beyond the capacity of traditional methodologies. In this field, AI is excellent. It can sort through data using complex algorithms to find patterns, correlations, and abnormalities that can escape human observers. This analytical skill is essential for various tasks, such as climate modelling, protecting animals, and reducing pollution.

Climate Prediction and Modelling:

Climate change is one of the most important environmental issues of our day. To better understand and anticipate the intricate dynamics of the Earth’s climate system, AI and ML are crucial to climate modelling. These technologies may analyze historical data, include real-time data, and simulate future events to enhance climate forecasts. Additionally, AI-powered models can improve the precision of climate impact assessments, assisting in creating policies for adaptation and mitigation. It makes it possible for communities, organizations, and government agencies to decide how best to protect themselves from the negative effects of climate change.

Protection of Biodiversity and Conservation:

A sustainable future depends on protecting biodiversity. AI is a strong ally in this effort, providing creative ways to stop invasive species, poaching, and habitat loss. For instance, camera trap photos can be identified and tracked using machine learning algorithms, offering important insights into endangered species’ behaviour and population dynamics. Additionally, AI-driven surveillance systems can quickly identify and take action in response to illicit activities, including illegal fishing, animal trafficking, and deforestation. It allows conservationists and law enforcement organizations to act quickly to safeguard sensitive habitats.

Optimization and the Circular Economy:

Managing resources effectively is essential to sustainability. AI enables resource use to be optimized across numerous industries. For instance, focused irrigation, insect control, and fertilizer applications using AI-powered precision farming techniques can increase crop output while reducing environmental impact. AI facilitates using circular economy ideas in waste management by streamlining recycling procedures and lowering waste production. Machine learning algorithms can help intelligent garbage sorting systems efficiently separate materials, maximizing the possibility of reuse and recycling.

Energy Efficiency and Renewable Integration:

In the shift to a sustainable energy environment, AI is crucial. Machine learning algorithms-driven “smart grids” improve the effectiveness and stability of energy distribution networks. These systems may seamlessly include renewable energy sources while dynamically adapting to shifting demand patterns. AI-driven predictive maintenance also aids in improving the efficiency of renewable energy assets like solar and wind power generators. Ultimately, this contributes to a more sustainable and robust energy infrastructure by extending their lives and ensuring maximum energy output.

Conclusion:

As environmental problems worsen, the fusion of AI with sustainability offers a glimmer of hope. We are in a position to fundamentally alter how we comprehend, oversee, and safeguard our planet by utilizing the analytical power of machine learning. These technological advancements provide a potent toolkit for developing original, data-driven solutions that will help to design a more sustainable future for future generations. A flourishing, resilient planet requires us to embrace AI to practise environmental stewardship.

Introducing artificial intelligence (AI) into financial operations has caused a paradigm change within the sector. AI has become a mainstay in the financial industry, with applications ranging from algorithmic trading to fraud detection and predictive analytics. This article examines how AI is transforming these three fundamental fields.

Financial Predictive Analytics:

Using AI algorithms in predictive analytics in finance enables the prediction of future consumer behaviour, market trends, and financial results. In the age of big data, conventional models frequently need help to process enormous amounts of data effectively. But by using machine learning algorithms, which can recognize patterns and make precise predictions, AI excels in this field.

1. Market Trends and Investment Strategies:

Market trends and investment strategies are identified using AI algorithms that examine historical market data, news sentiment, and macroeconomic factors. They continuously hone tactics and adjust to shifting market conditions to maximize returns for investors.

2. Risk management:

Predictive analytics powered by AI evaluate several risk characteristics, allowing financial organizations to make wise lending, investing, and portfolio management decisions. It increases stability and lessens exposure to unpredictable market volatility.

Fraud Detection and Prevention:

New types of fraud always threaten the financial industry. The ability of AI to evaluate enormous datasets and identify anomalies in real time has changed how fraud is detected.

1. Anomaly Detection:

AI systems can detect anomalies in transactional data and identify suspicious patterns that might indicate fraud. They are skilled at separating potentially fraudulent transactions from real ones.

2. Behavioral Biometrics:

AI can authenticate users using behavioural biometrics such as mouse movement patterns, keyboard dynamics, and voice recognition. This high level of security provides further defence against identity fraud and unauthorized access.

Automated Trading:

Algorithmic trading systems driven by AI carry out financial transactions at frequencies and speeds impossible for humans to match. To make split-second decisions, they use real-time data and sophisticated mathematical models.

1. Market Analysis and Strategy Implementation:

Market analysis and strategy implementation rely on AI algorithms that sift through enormous volumes of data to pinpoint the best points of entrance and departure. They execute deals precisely and react quickly to shifting market conditions.

2. Risk Management and Portfolio Optimization:

Risk management and portfolio optimization are two areas where algorithmic trading with AI places a strong emphasis. It uses strategies including stop-loss orders and dynamic portfolio rebalancing for a balanced risk-reward profile.

Issues and Moral Considerations:

Although the use of AI in banking has many advantages, there are also some difficulties. Critical considerations include ensuring transparency, preventing bias in decision-making, and defending against adversarial attacks. Regulatory organizations are currently establishing frameworks to control the moral application of AI in banking.

Conclusion:

Finance has entered a new era of efficiency, precision, and innovation due to the deployment of AI. Predictive analytics, fraud detection, and algorithmic trading are just the beginning of AI’s potential in this industry. Financial institutions must adopt new technologies responsibly as they develop, ensuring that they are used for the benefit of the sector and society.

Through the use of natural language processing (NLP), which enables computers to comprehend, decipher, and produce human language, healthcare has undergone a radical change. Although this technology has much potential for use in the healthcare sector, it also presents several unique difficulties. Here are some important NLP uses and problems in the medical field:

Applications of NLP in Healthcare:

1. Clinical Documentation Improvement (CDI):

Using NLP to extract data from unstructured text in medical records, clinical documentation can be made more accurate and efficient. Better coding, billing, and reimbursement procedures may result from this.

2. Clinical Decision Support (CDS):

NLP may examine medical literature, patient records, and other pertinent data to offer clinicians suggestions for diagnosis and therapy supported by the available scientific evidence. Adverse events, allergies, and possible drug interactions can all be helped to identify with this.

3. Information Extraction:

Clinical notes, radiological records, and pathology reports may be mined for specific information using NLP. One example is identifying important information such as diagnoses, treatments, prescription names, and dosages.

4. Voice Assistants and Chatbots:

NLP-powered voice assistants and chatbots can improve patient engagement while giving them access to basic medical information, appointment scheduling, medication reminders, and symptom checks.

5. Clinical Research:

Using a substantial body of clinical trial data and medical literature, NLP can assist researchers in extracting pertinent information for systematic reviews, meta-analyses, and cohort studies.

6. Sentiment Analysis and Patient Feedback:

Sentiment analysis and patient feedback are two areas where NLP can be used to monitor the calibre of care given and determine how satisfied patients are with the services received.

7. Disease Surveillance and Outbreak Detection:

NLP can process huge volumes of data from numerous sources (including electronic health records, news articles, and social media) to monitor and identify disease outbreaks in real time.

8. Language Translation:

By translating patients’ native tongues into the preferred language of the healthcare provider, NLP can make it easier for patients who do not speak English to communicate.

Challenges of NLP in Healthcare:

1. Data Security and Privacy:

Protecting patient privacy is vital because healthcare data is extremely sensitive. NLP systems must abide by stringent laws like the U.S.’s HIPAA (Health Insurance Portability and Accountability Act).

2. Data Quality and Variability:

Handwritten, abbreviated, misspelt, or highly specialised medical records might be difficult for NLP systems to process accurately.

3. Integration with Existing Systems:

Adding natural language processing (NLP) to current electronic health record (EHR) procedures and systems can be difficult, and interoperability problems could result.

4. Bias and Fairness:

NLP models may unintentionally reinforce biases in the training data, which could result in inequities in healthcare outcomes. There must be actions taken to lessen these biases.

5. Clinical Validation and Accuracy:

To ensure trustworthy information, NLP systems must undergo extensive examination for accuracy and clinical validity.

6. Lack of Standardisation:

It is difficult to develop standardised NLP models since medical terminology and language differ greatly among specialisations, geographic locations, and healthcare systems.

7. Continuous Learning and Updating:

NLP models for healthcare require constant updates to keep up with evolving medical terminology and expertise.

8. Ethics:

Using NLP has ethical ramifications, particularly in touchy contexts like mental health, end-of-life care, and genetic information.

Conclusion:

NLP can enhance healthcare, but issues need resolution for responsible integration into clinical practice. Collaboration between healthcare experts, data scientists, and ethicists is essential to navigate these challenges.

The recent Bernie Ecclestone case has put the limelight back onto Tax Fraud which is the scourge of the global economy as governments are losing billions of dollars in potential tax receipts. This short article will explore what is Tax Fraud, how it is executed and above all the measures to prevent it.

Tax Fraud is a serious offence that involves deliberately and dishonestly misrepresenting financial information on tax returns to evade or escape tax a liability. It ranges from under declaring income and inflating deductions to hiding offshore accounts. Tax Fraud is dangerous as it undermines the tax revenue collection system that ultimately undermines government fiscal policy, especially for essential services such as on education and health. The author believes detecting and preventing Tax Fraud is essential to maintaining a fair and equitable tax system.

Form of Tax Fraud

It can occur in a variety of ways, but it usually involves the following:

Underreporting Income: This is one of the most common forms of Tax Fraud and includes failure to report cash income, not declaring all business or trading income, or hiding assets that generate income. Next time a tradesperson or a professional offers the reader their service at a reduced fee if they do not want an invoice this should set the alarm bells ringing. Or if an establishment only accepts cash and no credit card transactions then there is strong possibility that they are committing Tax Fraud by not declaring all their income.

Inflating Deductions: Unfortunately, individuals or businesses exaggerate deductions to reduce their taxable income and will consequently incur a lower tax bill. Inflating business expenses, overstating charitable contributions or falsely claiming tax credits are some of the favoured techniques.

Offshore Tax Evasion: Taxpayers such as Bernie Ecclestone may attempt to hide assets and income in offshore accounts to avoid detection. This involves creating complex schemes, shell companies and offshore trusts. Tax practitioners may argue that they are simply exploiting loopholes in the national Tax Code and are merely helping clients to avoid tax. However, intent is crucial and the accounting convention of substance over form should be applied.

Ghost Employees: Employers may engage in payroll fraud by producing ‘ghost employees’ that do not exist or misclassifying workers as independent contractors to evade pay roll taxes, but the latter has largely been shut down by the imposition of IR35 in the UK.

Falsifying Documentation: Tax Fraud is underpinned by the creation of false documents such as invoices or financial statements to support fraudulent deductions or tax credits or genuine schemes to help for example new businesses.

Strategies to Fight Tax Fraud

The author believes that preventing Tax Fraud requires a combination of taxpayer education, enforcement, and regulatory interventions. These are his top ten strategies to fight Tax Fraud:

A Simplified Tax Code / System: Complex tax laws can have unintended consequences such as encouraging Tax Fraud. Simplifying the tax code will undoubtedly make it easier for taxpayers to understand and comply with the law.

Electronic Filing: Electronic filing systems can assist in reducing errors and enhancing the accuracy of tax returns. This will also enable tax authorities to engage in superior data analysis and predictive analytics.

Public Education: Educating the taxpayers regarding their obligations and the consequences of Tax Fraud is vital. Public awareness campaigns can help people and businesses understand the importance of accurate reporting and enhance the social contract between citizens and their government.

Robust Enforcement: Tax agencies must maintain a strong enforcement presence to deter potential fraudsters. Indeed, tax audits, investigations and penalties for tax evasion can help create a deterrence effect.

Regulating the Tax Profession: Regulation of tax agents or preparers or tax accountants cannot be left professional bodies such as the Chartered Institute of Taxation. There must be mandatory ethics training and licensing requirements to ensure an optimal profession. It is interesting to note that the term ‘Accountant’ is not protected in the UK and a taxi driver can become a tax accountant with little or no training.

Stronger Identity Verification: Implementing strong identity authentication measures can deter identity theft and fraudulent tax returns filed on the behalf of others.

Punishments: White-collar crime such as Tax Fraud may not lead to blood on the carpet, but it has socio-economic consequences such as lost opportunities to improve the health of a nation or help it make advances in science and technology. Therefore, there should be strict penalties for Tax Fraud, such as heavy fines and lengthy prison sentences. Prosecuting high-profile cases such as Bernie Ecclestone’s Fraud sends a strong message that this will not be tolerated.

International Agreements: There should be greater cooperation and formal international agreements between countries to fight the menace of offshore tax evasion.

Leveraging IT: Governments need to invest in IT such as helplines and chatbots to better assist companies and individuals so that they can better comply with legislation and reduce unintentional mistakes. In Sweden all tax returns including the Prime Ministers are available online for scrutiny.

Whistle-blower Lines: These are cheap and effective for people to report Tax Fraud as long they are anonymous and incentivised.

Conclusion

Tax Fraud remains an important issue that wrecks the integrity of tax systems across the globe and potentially cause severe socio-economic distress. Detecting and preventing Tax Fraud requires a multifaced approach that requires cooperation between government agencies, individuals, and businesses. By implementing strong enforcement measures, raising public awareness, simplifying national tax codes / systems, and effectively using advanced technology, governments can deter Tax Fraud and facilitate a fair and equitable tax system that benefits society at large.

Bonds are dynamically priced financial instruments. When they are issued initially, their price is indicated by their par value (or face value); however, later, the value of bonds is subject to factors such as the interest rate, credit ratings of the issue, liquidity in the market, or general economic and business aspects. Therefore, when buying bonds, investors need to carefully understand the theoretical price of the bonds and the possible implications of exogenous factors on the cost of a Bond.

Bonds’ Cash Flows

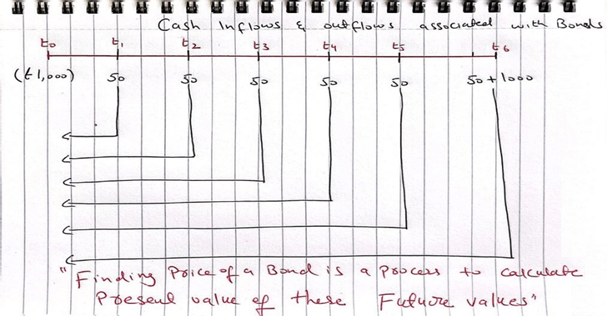

Bonds are long-term financial assets (debt instruments). The cash flows associated with these instruments are a time-based phenomenon. A bond investor, in essence, incurs a cash (£) outflow today to receive interest income and principal payments in future (Inflows). The example below explains the cash inflows and outflows associated with a bond maturing in 3 years, a par value of £1000, and an annual interest rate of 10%. The bond pays interest semi-annually; hence, the bond investor will receive £50 every 6 months. t0 means today, t1 means in six months, t2 means in 12 months, and so on (please see the picture below).

Source: Author’s creation.

Therefore, a bond purchase is an exchange of money today against promised money in the future. Accordingly, to find a bond’s value (price), we must calculate the present value of these future cash inflows (as depicted below).

Source: Author’s creation.

The bond valuation can be done using the following formula.

Coupon payment = Interest rate offered by the bond.

[coupon payments are calculated by considering if they are paid annually, semi-annually, or quarterly]. For example, an annual interest rate of 10% means a 5% semi-annual rate, which is calculated as 10%/2. If it was monthly, then we divided 10% by 12.

r = discount date or required rate of return by the company.

n = periods to maturity.

Principal payment = par value, which the investor paid at the beginning.

Another way of approaching this is the following equation, where we discount all the cash flows individually and then sum up the discounted cash inflows to estimate the present value of future cash flows.

Example:

Bond A

Bond B

Maturity (years)

50

20

Coupon rate (%)

9

8

The interest rate paid on the principal (paid semiannually)

Par Value/Face Value/Book Value

$1,000

$1,000

Find price and tell whether they are selling at premium or discount.

Solution:

Price of Bond A

Price of Bond B

Both bonds are selling at a discount value.

Principles of Bond Pricing

The price of a bond is the function of the future cash flows associated with the bonds and their certainty. The first requires bond issuer to offer a rate that is better than the alternative investment rate (required rate of return). The second refers towards default risk premium.

The required rate of return discounts the future cash flows to the present to establish their present value. Therefore, the present value of cash flows associated with a directly depends upon the discount rate (required rate of the investors). Therefore, the discount rate is the primary determinant of the value of the bonds. The relationship between bond prices and the required rate is inverse. As the required rate goes up, the price of the bond decreases.

However, the question of how this required rate is determined. This rate is determined by the interest rate set by the Bank of England in the UK or the Federal Reserve Bank in the USA. This rate is also known as the risk-free rate and is one of the most important variables in our economy.

Furthermore, it’s also important to remember that the relationship between risk-free rates and bond prices is inverse; as the interest rate increases, the bond price decreases. Risk free rate of a country is influenced following four forces:

Inflation Levels and future expectations about inflation levels. The higher the inflation level and future expectations, the higher the risk-free rate.

Economic Growth or national levels of output. The slower the Growth, the lower the risk-free rate, and vice versa.

Quantity supply of money or, in other words, how much money the Bank of England prints. The relationship is convex and shows the complexity and sensitivity with which central banks need to deal with this problem.

Fiscal situation of a country. Suppose a country is in deficit and needs to borrow more money. As a result, the risk-free rate increases and vice versa.

Default Risk Premium refers to the credit risk associated with a bond issuer. The risk indicates whether an issuer can make the promised future payments on time. This risk depends on an issuer’s ability to generate revenues or sales. An issuer in a growing economy is more likely to make future payments and vice versa. Therefore, Bond issuers must offer an interest rate that compensates for default risk or may have to sell the bond at a discount.

References

Mishkin, F. S., & Eakins, S. G. (2019). Financial markets. Pearson Italia.

Madura, J. (2020). Financial markets & institutions. Cengage learning.

Pilbeam, K. (2023). International finance. Bloomsbury Publishing.

Fabozzi, F. J., Modigliani, F., & Jones, F. J. (2010). Foundations of financial markets and institutions. Pearson/Addison-Wesley.

Kaufman, H. (1994). Structural changes in the financial markets: economic and policy significance. Economic Review-Federal Reserve Bank of Kansas City, 79, 5-5.

Kaufman, H. (2009). The road to financial reformation: Warnings, consequences, reforms. John Wiley & Sons.

Kaufman, H. (2017). Tectonic Shifts in Financial Markets: People, Policies, and Institutions. Springer.

Hunter, W. C., Kaufman, G. G., & Krueger, T. H. (Eds.). (2012). The Asian financial crisis: origins, implications, and solutions. Springer Science & Business Media.

Glushchenko, M., Hodasevich, N., & Kaufman, N. (2019). Innovative financial technologies as a factor of competitiveness in the banking. In SHS Web of Conferences (Vol. 69, p. 00043). EDP Sciences.

Kaufman, G. G. (2002). Too big to fail in banking: What remains?. Quarterly Review of Economics & Finance, 42(3), 423-423.

Kaufman, G. G. (2000). Banking and currency crises and systemic risk: Lessons from recent events. Economic Perspectives, 24(3), 9-28.

Diamond, D. W., Kashyap, A. K., & Rajan, R. G. (2017). Banking and the evolving objectives of bank regulation. Journal of Political Economy, 125(6), 1812-1825.

Corporate bonds are promissory notes that large firms issue to raise long-term and short-term debt. These bonds are issued with either an attached coupon or with no interest rate but a discounted price. They are issued in denominations (face value) of $1000 and pay interest twice yearly (semi-annual). These bonds enable firms to raise capital at a lower cost and provide flexibility.

However, unlike government bonds such as T-bills issued by the USA or gilts issued by the UK government. Corporate bonds carry “default, payment, and interest rate risk” for their investors—the degree of risk and its nature changes based on who is issuing the bond. If APPLE Plc issues the bonds, its risks are much different from those of a firm based in India. Because both firms’ operations, income currency and credit ratings are foreign.

Default risk means that a borrower may default before or even on the maturity of the bonds. Bonds are forward promissory notes, meaning the principal you invest today will be due in future. For example, a $1000 -10-year bond with a 10% coupon rate would result in two payments: a principal amount of $ 1000 at the end of year 10 and an annual fee of $100 (10% of 1000) at the end of every year. After making the 7 interest payments to you, the firm may go bankrupt or dissolve, so you may never receive your principal.

Payment risk refers to the risk that the bond issuer cannot pay their annual or semi-annual interest payment. For example, during Covid-19, many firms like airlines could not earn any income. As a result, they required a “payment holiday” during the covid year. Therefore, an investor investing in corporate bonds should be ready to handle payment risk.

Interest rate risk: the bond price is inversely related to the interest rate set by the central banks. Therefore, if the interest rate goes up (like nowadays), the value of the bond will start to go down. This means that if, as an investor, you wish to sell the $1000 bond now rather than waiting for 10 years of maturity, you may have to sell it for a price lower than $1000.

Exchange rate risk is caused by exchange rate volatility. If you invest in foreign currency bonds such Indian rupee or KSA rials, you may lose money to the value of £ appreciates due to a change in the exchange rate. Because now, for the same units of foreign currency, you may get a lower £. However, this can also become a source of extra income if the value of £ decreases.

Call risk:Bondholders also need to manage the call risk, whereby the bond terms give the company the right to buy back the bond before the maturity date. This risk represents a lost income risk for the bond investors.

Liquidity risk: liquidity risk refers to the lack of demand for a particular bond. Bondholders may need help selling their bonds or may have to sell them at a heavily discounted price.

Interest rate risk refersto the risk of a fall in bond prices whereby a rise in interest rate leads to lower bond prices. For example, as interest rates have recently increased, bond values have begun to fall rapidly.

Inflation risk refers to the fall in the value of a bond’s principal or interest payments. The fall happens as the real value of future cash flows declines due to higher inflation. In other words, inflation over time means the money received on the bond’s interest and principal payments will purchase fewer goods and services than before.

Credit Quality of Corporate Bonds

Bonds, especially corporate ones, must demonstrate to their investors that they are of good quality and would deliver the maximum value for investors’ money. Good quality means three things: 1. There’s clear evidence of a firm’s creditworthiness and certainty that there are no defaults and payment risks to the investors. 2. Bondholders can see the protection against the agency conflict, indicating enough covenants to inhibit management from using the borrowed money for the wrong reasons. The agency conflict emerges due to information asymmetry, moral hazard problems, and adverse selection problems. 3. Cushion against systemic risks and macroeconomic universities such as interest rate rises, exchange rate risks, or political and war risks. Therefore, the corporate bonds issued by the firms indicate their quality to the firms by changing the characteristics of bonds. These issuers must also use third parties like rating agencies to tell their credit quality.

Corporate Bond types based on their Credit Ratings

Rating agencies like Moody’s, Fitch, and S&P rate firms and their issued bonds. These agencies may give credit ratings after solicitation with the bond issuer or without any solicitation. The associated credit ratings often indicate corporate bonds’ riskiness. Bonds deemed lower risk bonds usually have higher credit ratings, such as AAA or AA+. The higher-risk bonds are generally junk bonds, and their ratings are below BBB-. The interest rate charged to higher-rated bonds differs from lower-rated bonds. However, other than credit ratings feature of bonds such issuers’ leverage ratio, coverage ratios, and assets, etc. Based on the credit ratings, we can broadly categorise bonds into the following two types:

Investment Grade Bonds: Bonds rated Baa or better by Moody’s and BBB or better by S&P are considered investment grade bonds.

Junk Bonds: Theseare bonds with credit ratings lower than BBB– also called speculative grade bonds. These bonds are also called junk or high-yield bonds. A junk bond is a risk investment that is likely to default. In comparison, the default risk of investment-grade bonds is negligible.

Understanding Corporate Bonds and their Characteristics

What are the characteristics of corporate Bonds?

Bond characteristics are the terms, covenants, and restrictions attached to a bond. For example, a standard bond would have a face value of $100, mature 10 years, and have an interest rate of 10% paid semi-annually. Therefore, it means the bond will pay you upon maturity $100. The bond will mature after 10 years, and the interest payment will be $50 after 6 months (1000 * (10%/2)).

Corporate bond issuers often use the bonds’ characteristics to indicate the bond’s credit quality to the investors. The following are the major characteristics of corporate bonds firms use to show their credit quality.

Restrictive/Protective Covenants: an issuer may use certain conditions to ensure bond investors will not suffer from “agency of conflict”. These covenants provide that managers do not make money for themselves or the shareholders at the expense of bond investors. These covenants limit the management by putting constraints on the following:

How much dividends can management pay to ensure enough cash reserves for interest payments?

How much additional debt (bonds) can the firm issue to ensure they stay manageable with debt?

The seniority of the later debt issuance, which ensures that bonds issued later would be after the existing bondholders are paid in full.

Restrictive covenants mean that bondholders are well protected, and as a result, these bonds usually offer lower interest rates.

2. Call Provision: Call provision refers to an issuer has right to force the bond holder back earlier than its maturity. There is a grace period before which an issuer may call; however, after this call, they can call the bond at either face value or higher than market price as part of bond terms and conditions. The issuer can also call part of their total bond stock (such as only 10% of issued bonds are called). Doing so gives the investor confidence that the firm is generating sufficient cash. Furthermore, the probability of default decreases. The firm becomes safer as its overall debt decreases.

A call provision is also put in place that if a firm decides to engage in an activity not viewed favourably by investors, then the firm can pay back those bondholders and continue with their business. For example, if a bond covenant restricts firms from investing in an emerging economy. The management views investing in an emerging economy as compelling; they can continue after paying the bondholders in full.

Firms also use call provision to manage their capital structure. The debt-to-equity ratio is very low if they feel that existing bond levels make their firm too indebted. Then, they may force bondholders to sell their bonds to reduce the level of debt and improve their financial risk profile and creditworthiness.

However, the call provisions ensure that management fully controls its debt and debt management. Nevertheless, these provisions are viewed negatively; bondholders want higher interest rates for bonds with call provisions.

3. Conversion: Some bonds allow bondholder to convert their bonds into stocks/shares if they prefer. This characteristic allows the bondholders to benefit if the firm’s share prices have increased. The convertibility provision states the number of shares the bondholders can claim for one bond. The convertible bonds signal to the market about a firm’s prospects.

If management believes the firm’s share prices will increase, they may issue a convertible bond. Therefore, bond investors like such bonds as it gives them the best of both worlds.

4. Secured Bonds: These bonds have collateral attached to them. The collateral can be property, equipment, land, or other fixed assets. These bonds usually finance a predefined project or specific business capital expenditures. The bondholder can liquidate the property or asset if firms do not make interest or principal payments. These bonds are assumed to be safer and have lower interest rates. Similarly, firms may issue equipment trust certificates against non-real estate assets such as heavy equipment and aeroplanes

5. Unsecured bonds: Firms can issue unsecured bonds having attached a customised set of terms and conditions. These terms and conditions, indenture, show both parties’ rights and responsibilities to a bond issue (firms and bondholders). They are risky assets with a higher interest rate; however, payment priority is the last in case of default.

6. Credit Ratings: firms can also use the rating agencies to indicate their firm’s credit quality and the credit quality of their issued bonds. The ratings, such as the AAA to D scale, show the firm’s creditworthiness.

7. Financial guarantees: Sometimes, bond issuers purchase financial securities such as insurance against the event of default. This guarantee ensures that borrowers can get their principal and interest payments. This guarantee is issued by large banks such as JP Morgan or Bank of America. Therefore, borrowers can handle the quality of the bond issuer. Instead, they would look at the insurer’s quality and consider the issued bonds good quality. These insurance instruments are called “Credit Default Swaps (CDS)”. These instruments are traded and allow investors to secure their bonds.

Types of Corporate Bonds based on their Characteristics

The following are the main types of bonds firms use to raise capital.

Secured Bonds.

Unsecured Bonds – Debentures.

Unsecured Bonds – Convertibles

Unsecured Bonds – Debentures.

Unsecured Bonds – Subordinate Debentures.

Unsecured Bonds – Variable rate bonds.

Unsecured Bonds – Puttable Bonds.

Investment grade and Junk (speculative) grade Bond

Mortgage-Backed Securities

References

Mishkin, F. S., & Eakins, S. G. (2019). Financial markets. Pearson Italia.

Madura, J. (2020). Financial markets & institutions. Cengage learning.

Pilbeam, K. (2023). International finance. Bloomsbury Publishing.

Fabozzi, F. J., Modigliani, F., & Jones, F. J. (2010). Foundations of financial markets and institutions. Pearson/Addison-Wesley.

Kaufman, H. (1994). Structural changes in the financial markets: economic and policy significance. Economic Review-Federal Reserve Bank of Kansas City, 79, 5-5.

Kaufman, H. (2009). The road to financial reformation: Warnings, consequences, reforms. John Wiley & Sons.

Kaufman, H. (2017). Tectonic Shifts in Financial Markets: People, Policies, and Institutions. Springer.

Hunter, W. C., Kaufman, G. G., & Krueger, T. H. (Eds.). (2012). The Asian financial crisis: origins, implications, and solutions. Springer Science & Business Media.

Glushchenko, M., Hodasevich, N., & Kaufman, N. (2019). Innovative financial technologies as a factor of competitiveness in the banking. In SHS Web of Conferences (Vol. 69, p. 00043). EDP Sciences.

Kaufman, G. G. (2002). Too big to fail in banking: What remains?. Quarterly Review of Economics & Finance, 42(3), 423-423.

Kaufman, G. G. (2000). Banking and currency crises and systemic risk: Lessons from recent events. Economic Perspectives, 24(3), 9-28.

Diamond, D. W., Kashyap, A. K., & Rajan, R. G. (2017). Banking and the evolving objectives of bank regulation. Journal of Political Economy, 125(6), 1812-1825.

We will discuss these types in detail in another article.